Personal financial knowledge has become an important aspect of an individual’s life. It involves having an understanding of one’s financial situation and making informed decisions about matters of money.

A major aspect of personal financial knowledge is budgeting. This involves planning how to spend money and sticking to that plan. A budget helps to prioritize the spending and avoid overspending.

The second important aspect of personal financial knowledge is saving. It involves putting aside some money for future use, maybe for emergencies, retirement, or other long-term goals. This provides a sense of security and helps to achieve financial goals.

Investing is the third key component of personal financial knowledge. It means putting money into investments such as stocks, bonds, or real estate with the goal of earning a return on investment. Understanding investing can be complex, but it is important to grow wealth over time.

And finally, having knowledge of credit and debit is crucial for personal financial success. This includes understanding how credit scores work, managing credit card debt, and avoiding high-interest loans.

In addition to the above mentioned aspects, personal financial knowledge also includes understanding taxes and insurance. Tax planning is crucial as it helps to minimize tax liability and maximize refunds. Insurance knowledge helps to protect assets and safeguard financial future against unforeseen events.

Moreover, personal financial knowledge also involves understanding one’s financial goals and risk tolerance. This helps individuals to make informed investment decisions that align with their objectives and risk appetite.

Overall, developing personal financial knowledge is a process that requires education and practice. By taking the time

to learn about budgeting, saving, investing, and credit, individuals can make informed decisions and achieve their financial goals.

It is important to note that personal financial knowledge is not just limited to individuals who earn a high income. It is equally important for individuals with low or moderate income to have a good understanding of personal finance. In fact, having personal financial knowledge can help individuals with limited income to make the most of their resources and achieve their financial goals.

The US dollar (USD) and the Chinese renminbi are two of the world’s most widely used currencies. As the world’s two largest economies, the United States and China, both countries use their currency to trade with other countries and conduct international transactions.

The US dollar has been the world’s dominant currency since the end of World War II. It has been used as the international reserve currency, meaning that central banks around the world hold USD as a means of payment for international trade and investment. The Chinese renminbi, on the other hand, has only become a major international currency in the last few decades. Until 1994, it was pegged to the USD at a fixed exchange rate. However, China has since moved towards a more flexible exchange rate system, allowing the Renminbi to appreciate against the USD.

Renminbi (RMB) and yuan are two terms that are often used interchangeably to refer to the Chinese currency. However, there is a slight difference between the two terms.

Renminbi, which translates to “people’s currency” in English, is the official name of the currency used in China. Yuan, on the other hand, is a unit of the renminbi currency. It is the basic unit of the currency and is used to express the value of goods and services in China.

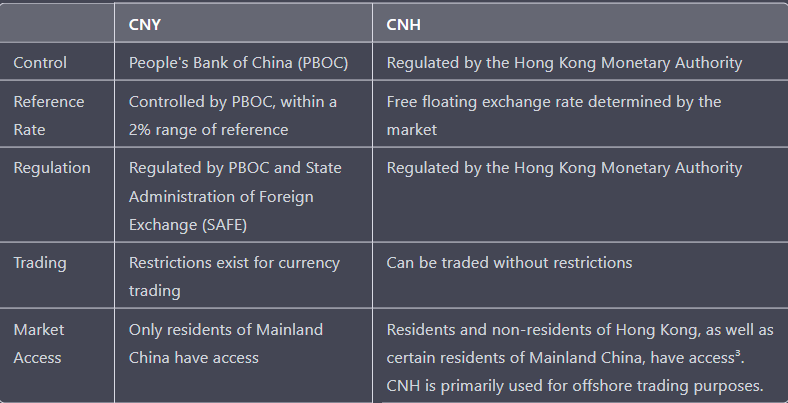

There are two types of Renminbi, which implies two types of Yuan: CNY and CNH. CNY is the Chinese Yuan that is traded within the country’s borders, while CNH is the Chinese Yuan that is traded offshore. While CNY and CNH have the same value in Renminbi, they are distinct currencies that are subject to different levels of regulation and restrictions and are traded at different prices. CNY is regulated by the People’s Bank of China, while CNH is regulated by the Hong Kong Monetary Authority. Despite some similarities, they are not the same currency.

Before 2005, the yuan was fixed to the US dollar at a rate of 8.27 yuan per USD but was then revalued to 8.11 yuan/USD. China has been gradually promoting the international use of the yuan by making foreign trade in the currency more efficient and flexible. Since 2006, the renminbi has been operating under a managed floating exchange rate system. Its value is based on a basket of currencies and allowed it to fluctuate within a narrow range. However, the exchange rate is reset daily based on supply and demand, with the central bank setting a daily reference rate that allows the currency to move within a 4% band around the reference rate, ignoring the previous day’s trading activity. Over the next three years, the yuan was allowed to appreciate by about 21% to a level of 6.83 to the dollar. In July 2008, China halted the yuan’s appreciation as worldwide demand for Chinese products slumped due to the global financial crisis. In June 2010, China resumed its policy of gradually moving the yuan up, and by august 11,2015, the yuan had appreciated by 33% against the US dollar . On August 11, 2015, the People’s Bank of China (PBOC) surprised markets with three consecutive devaluations of the Chinese yuan renminbi (CNY), knocking over 3% off its value. After a decade of steady appreciation against the U.S. dollar, investors had become accustomed to the yuan’s stability and growing strength. The drop amounted to 4% over the subsequent two days. Stock markets in the U.S., Europe, and Latin America also fell in response to the yuan devaluation. Most currencies also reeled. It is speculated that the devaluation was done as a desperate attempt to stimulate China’s sluggish economy and keep exports from falling further, as the devaluation occurred just days after data showed a sharp fall in China’s exports—down 8.3% in July 2015 from the previous year. However, PBOC claimed that the devaluation’s purpose was to allow the market to be more instrumental in determining the yuan’s value more believable. The PBOC stated that this was a one-off devaluation and the move was intended to bring the yuan’s central parity rate closer to market rates, allowing the market to play a greater role in determining the exchange rate. The ultimate goal was to deepen currency reform and make China’s currency system more market-oriented. this was in line with the Chinese Republican party pledge to make the renminbi a global reserve currency after the International Monetary Fund (IMF) added the yuan to its Special Drawing Right basket on Oct. 1, 2016. This basket initially included the euro, Japanese yen, British pound, and U.S. dollar. The SDR is an international reserve asset that IMF members can use to purchase domestic currency in foreign exchange markets to maintain exchange rates. The IMF reevaluates the currency composition of its SDR basket every five years. In 2010, the yuan was rejected on the basis that it was not freely usable. The IMF welcomed the devaluation, encouraged by the claim that it was done in the name of market-oriented reforms. Consequently, the yuan became part of the SDR. After this yuan stabilized and was contained between 6 yuan/dollar and 7 yuan/dollar. With the little variation caused due to various factors like –

Economic Growth: Economic growth in both the US and China can impact the exchange rate. If China’s economy grows faster than the US, demand for CNY may increase, causing its value to appreciate against the USD.

Trade Balance: The trade balance between the two countries can also affect the exchange rate. If China exports more goods to the US than it imports, it will accumulate more USD, which can put downward pressure on the CNY. Conversely, if China imports more goods from the US than it exports, it will accumulate more CNY, which can put upward pressure on the currency.

Monetary Policy: Monetary policy decisions by the US Federal Reserve and the People’s Bank of China can also impact the exchange rate. Changes in interest rates or other monetary policy tools can affect the value of the USD and CNY relative to each other.

this recognition by IMF gave china various benefits like increased international contracts priced in yuan, which reduced its reliance on the US dollar and mitigated exchange rate risks and transaction costs. Furthermore, central banks were required to hold yuan as part of their foreign exchange reserves which boosted demand for the currency and lowered interest rates for yuan-denominated bonds. This resulted in lower borrowing costs for Chinese exporters and strengthened China’s economic clout relative to the United States, supporting President Jinping’s economic reform agenda.

While going through Economic Times in our local newspaper, we all might have stumbled across the word Forex Exchange Market but what is it? Now and then we hear the news that the Indian currency has gained value against US Dollar but who decides this? Is there a guy on the computer generating these exchange rates randomly as per his whims…. fortunately, the answer is a big NO! These rates are decided by the foreign exchange market, the Forex or FX market which is a global decentralized marketplace where currencies are bought and sold. It is the world’s largest and most liquid financial market, with daily transactions worth trillions of dollars. In this blog, we’ll take a closer look at the foreign exchange market, including its importance, how it works, the factors that affect it, and the risks involved.

What is the foreign exchange market?

The foreign exchange market is where currencies are traded. Its participants include large international banks, corporations, hedge funds, individual investors, and central banks. Transactions can be on the spot (immediate delivery) or can be forwarded (delivery at a future date) and are typically conducted over-the-counter (OTC), meaning they are not traded on an exchange. Since currencies are always traded in pairs, the foreign exchange market does not set a currency’s absolute value but rather determines its relative value by setting the market price of one currency if paid for with another. The most actively traded currencies are the US dollar, Euro, Japanese Yen, British pound, and Swiss franc.

Factors affecting the foreign exchange market

Several factors affect the foreign exchange market, including economic, political, and other factors. Economic factors that impact exchange rates include interest rates, inflation, and economic growth. For example, if a country’s interest rates increase, its currency tends to appreciate because investors will earn higher returns on their investments. Political factors such as government stability and international trade policies can also impact exchange rates. Natural disasters and geopolitical tensions are other factors that can also affect the foreign exchange market.

How the foreign exchange market works

The foreign exchange market works through the interaction of supply and demand for currencies. Exchange rates are determined by the market’s participants, who are constantly buying and selling currencies. Currency pairs, such as USD/EUR, are used to indicate the value of one currency in relation to another. Banks serve as intermediaries between buyers and sellers, while central banks are responsible for regulating the currency supply and interest rates. Corporations use the foreign exchange market to manage their exposure to foreign currencies, while individual traders speculate on exchange rate movements. Some of the transaction methods are:

1)Spot Transaction

A spot transaction is a two-day delivery transaction, incontrast with the future contracts, which are usually three months. This trade represents a “direct exchange” between two currencies. It has the shortest time frame, involves cash rather than a contract, and interest is not included in the agreed-upon transaction

2)Forward Transaction

One way to deal with foreign exchange risk is to engage in a forward transaction. In this transaction, money does not actually change hands until some agreed-upon future date. A buyer and seller agree on an exchange rate for any date in the future, and the transaction occurs on that date, regardless of what the market rates are then. The duration of the trade can be one day, months, or years.

3)Swap

The most common type of forward transaction is a Swap in which two parties exchange currencies for a certain length of time and agree to reverse the transaction at a later date. These are not standardized contracts and are not traded through an exchange. A deposit is often required to hold the position open until the transaction is completed.

4)Option

A foreign exchange option is a derivative where the owner has the right but not the obligation to exchange money denominated in one currency into another currency at a pre-agreed exchange rate on a specified date.

Risks associated with the foreign exchange market

There are several risks associated with the foreign exchange market.

Market risk is the risk of loss due to exchange rate fluctuations.

Credit risk is the risk of default by one of the parties involved in a transaction.

Operational risk is the risk of loss due to errors or failures in operational processes, such as settlement or clearance.

Legal risk is the risk of loss due to legal disputes or regulatory changes.

Conclusion

The foreign exchange market is a complex and dynamic marketplace that plays a vital role in the global economy. It enables the exchange of currencies between countries, allowing for international trade and investment. Understanding the foreign exchange market is essential for businesses and investors looking to manage their exposure to foreign currencies. However, it’s important to be aware of the risks involved and to take appropriate measures to manage them.

It is not just the health of the masses that the coronavirus pandemic has hit, but almost all the aspects of normal life. Businesses, markets etc., are no different and have received a big blow. Profits plummeted, and most companies were pushed to run in losses making some companies bankrupt too. However, there were some businesses, startups that not only managed to stay afloat but thrived in these times of crisis. Innovation being a key to beat the covid blues. There was a myriad of opportunities for new-age startups and investors to tap into, given the rise in demand for a variety of services . A bull market is a term for the stock market when the securities rise, and a bear market is when securities fall for a sustained period. This blog focuses on those Indian based or originated startups, businesses, newly turned unicorns etc., who developed and flourished in this pandemic, when most of the economy was about to hit rock bottom, thus becoming bulls of the bear Indian market.

Healthcare

Healthcare was an industry that constantly had hopes hooked to it in the pandemic. Doctors, nurses, medical professionals were the need of the hour. From the business point of view, pharmaceutical companies, telemedicine, online medical consultations etc., had profits jumping many folds. The startups that prospered in the healthcare sector were:-

Serum Institute of India:- With net sales of INR 5,446 crores amidst the COVID-18, Serum earned a net profit of INR 2,251 crore. Or a net margin of 41.3%. Serum Institute of India the vaccine manufacturer that has become pivotal to India’s recovery from this pandemic.

Practo:- Practo reported a 500% spike in online medical consultation under lockdown.

PharmEasy:- E-pharmacy is the most important e-commerce sector in this ongoing pandemic. Due to home confinement, people are finding it very inconvenient to get their prescriptions and over the counter (OTC) medicines, so instead, they switched to telemedicine like PharmEasy, Netmeds etc.

Bioline:- Based in Indore, Bioline India was founded by Neeta Goel and her late husband Rajeev Goel in 2001 to manufacture and supply affordable medical equipment to the masses. During COVID-19, the demand skyrocketed for this once slow-moving product.

Zyro care:- Kamayani Naresh, a retired Indian Navy officer, claims to have developed a long and sustainable solution to boost immunity — zyropathy. A Delhi-based company that provides food and herbal supplements.

Education

With schools shut down all across the globe, the education sector underwent quite a revolutionary state. The education system required expeditious reforms to avoid the education of thousands of students coming to a standstill. EdTech startups saw a boom in their market. Online classrooms and courses came to students’ rescue. The businesses that burgeoned in the education sector were.

Unacademy:- Unacademy beat the pandemic to enter the prestigious list of unicorns in India. The EdTech firm raised around Rs 1,125 crore in a funding round led by Softbank Vision Fund 2 and participation from existing investors, including Facebook.

Byju’s:- Byju’s is one of the top e-learning startups of India, which is surpassing all its competitors and has become one of the few decacorns in Indian startup history after crossing $10.5 Billion valuations in the midst of this pandemic.

Gradeazy in Surat:- After their first startup had a false start in 2018, Surat-based Dishant Gandhi and Alok Kumar found a new opportunity to satiate their hunger for entrepreneurship with EdTech when the lockdown started, and all the schools and education moved online. The duo launched Gradeazy in June 2020 to enable educational institutes to conduct online examinations for just Re 1 per exam.

Media and Entertainment

With the freedom to go out and carry our daily routines being curbed, it was evident that people were going to turn to TVs and other platforms to while away the extra time in hand. The media and entertainment industry in India put up a great show in 2020.

Dailyhunt:- News and content aggregator Dailyhunt has become India’s first tech unicorn focused on vernacular content after raising $100 Mn funding from Google, Microsoft and Falcon Edge’s Alpha Wave Incubation at a unicorn valuation.

Khabri:- In one of the newest startups, which was launched in October 2017, Khabri is India’s first and the fastest growing digital audio platform. Khabri provides audio content in regional languages where anyone can create, listen or discover in the app. As a great initiative, Khabri has introduced the COVID-19 helpline for the visually impaired population of India as a massive outreach program.

According to Inc42 Plus, the media and entertainment sector received a total funding of $877.8 Mn across 85 funding deals last year, compared to $561.27 Mn in 2019, led by online video startups like SimSim, Trell and other TikTok alternatives.

NeeStream:- A popular OTT platform in South India. With several new films being released on the platform, NeeStream has been witnessing a rise in subscriber numbers.

Finance and Technology(FinTech)

Razorpay:- Bengaluru-based payments gateway Razorpay entered the unicorn club in October 2020 when it raised $100 Mn in its Series D round, led by GIC and Sequoia Capital India. The funding round also saw participation from the company’s existing investors, such as Ribbit Capital, Tiger Global, Y Combinator and Matrix Partners.

Pine Labs:- Noida-headquartered Pine Labs became the first unicorn for the year 2020, after its corporate round in January, led by New York-based financial services major Mastercard. Founded in 1998 by Lokvir Kapoor, Pine Labs provided its services to over 100K merchants in 3700 cities and towns across India.

Zerodha:- Bengaluru-based Zerodha was founded in 2010 by Nithin and Nikhil Kamath and offers stockbroking services. The company has claimed to have over a million active clients who trade and invest and is now valued at around 7000 crores or 1 billion approx.

E-commerce

A study showed that Indian e-commerce grew 84% in 4 years owing to the Covid-19 impact. When it was not possible to go out shopping, products were brought to individual doorsteps. A giant boom in local, national and international e-commerce startups is a testimonial to it.

Flipkart:-Flipkart witnessed new user growth of close to 50 per cent soon after the lockdown.

Bigbasket:-Bigbasket has had a huge inflow of orders as more and more consumers are preferring to order essentials and groceries online amid COVID-19. Bigbasket has added around 10,000 new workers to meet the massive influx of orders, which shows the shift to digital platforms in need of the millennium.

Custkartin Bokaro:-Custkart has its own factory near Bokaro that produces merchandise, and all the workers come from the nearby villages.

Miscellaneous

Nykaa:- Mumbai-based omnichannel lifestyle retailer Nykaa entered the unicorn club after raising around $13.6 Mn from its existing backer Steadview Capital. The funds were raised as part of Nykaa’s Series F funding round.

Cars24:- Gurugram-based online used car marketplace Cars24 entered the unicorn club by raising $200 Mn in a Series E funding round led by DST Global.

Rooter:- One of India’s biggest Sports community platforms, Rooter has raised $1.7 million (~ Rs 12.4 crore) in a pre-series A funding round at a time when almost all sporting activities have been seized across the globe. The Esports platform plans to capitalise on its upcoming Esports and gaming content and communities. Rooter engages its fans with user-generated live audio and video content.

Gaming

Paytm First Games registered a 200% increase in user base.

After the ban on the popular Chinese short-video app TikTok under 69A of the IT Act, its alternatives, including Trell, ShareChat, Chingari, Bolo Indya, Mitron, Roposo, Moj and Josh, among others, started gaining massive popularity and traction in the market.

Games like FAU-G, Mask Gun and others emerged as alternatives for many users in India after PUBG Mobile’s ban.

Podcasting

India is witnessing an unprecedented boom in podcasts, and it is a country with 22 modern Indian languages and around 720 recognized dialects. The linguistic diversity in India is increasing the demand for the information available on various platforms in vernacular languages. With a growth rate of 33 per cent, the vernacular internet ecosystem in the country is thriving.

The pandemic has an impact on economies and businesses throughout the world and will keep doing so for even some time in the future. It is no doubt now that opportunities can be squeezed even from the most diabolical of times. The pandemic has proved to be both an edge or stumbling block for establishments and enterprises across the globe. 2020 was a year of crisis, and crisis is where innovation thrives.

We are in the middle of a crisis. Not just the Covid-19, but the psychological turmoil of making money from every single dime available, even if it costs the whole economy’s meltdown. Does the short term or long term recession teach a lesson and put an end to this? It doesn’t seem so.

Something similar happened in mid-2008, whose foundations were laid in America’s housing market and the whole world had to face the consequences.

We’ll go step by step, starting from understanding the housing system and how it all collapsed. Don’t get muddled by the terms used ahead, as the concepts behind those are simple. The wall street people use these terms to keep the common people out of their way.

The Housing System

You must be familiar with the term mortgage. In case you are not, visualize it like this- you want to buy a $100,000 house, but you have only $30,000 with you. You approach a bank and ask for a loan. You pay $30,000 as a down payment, the bank lends you the rest of the money and based on your net worth, income statement, etc. bank decides a term of repayment and a reasonable rate of interest. Let’s assume this rate to be 10%. The bank allows you to pay it off in 30 years as monthly installments.

The house here represents a mortgage. Every month as you pay off the mortgage, you own the house a bit more and the bank owns a bit less. That’s how you own the house entirely after 30 years, and it’s no more a mortgage. And as the housing and real estate market is always soaring, real estate prices will always rise, as assumed before the crisis.

So your wealth will still be increasing even though you have to pay interest on the mortgage to the bank. It’s a win-win situation for all.

Building The Castles Of Money

Banks don’t always keep these mortgage bonds to themselves. They sell it to big investment banks and earn a nice commission. So the interests that you were paying on your loan went to their pockets now. But these small transactions didn’t keep the adrenaline of the big banks and investors running. So they came up with the idea of Securitization Food Chain. The idea was to bundle thousands of these mortgages on home loans along with mortgages on several other loans and sell it all together. This way, the yields will go up, and they assumed the risk to be still low as the housing market was always considered vital. They called it Mortgage-Backed Securities (MBS). The deal sounded like music to the ears of investors. So the investors all over the world leveraged lumps of money and invested heavily in these MBS, packed in a small magical box: a CDO.

A CollateralizedDebt Obligation or a CDO classified the above- mentioned mortgage bonds as per their risk of returns, the risk of trusting people that they will pay their mortgage on time. The ones who have a nice flow of income have a low risk and are rated AAA. Below them are AA, BBB, and the worst are BB-rated. BB refers to the houses owned by highly irresponsible people who hardly deserve to get a loan. These BB-rated mortgages are referred to as Sub-prime Mortgages. All these ratings are given by separate rating agencies that played a significant part in setting the crisis’s blueprint.All these bonds are then further sold to investors at a nice profit. The whole system was great because almost everyone earned a good profit and kept their cashflow running until things took an ugly turn.

The Inflation Of Real Estate Bubble

As the investors were earning good returns and demanded more MBS to invest in, but they couldn’t find any because most of the ‘eligible’ families already had a mortgage. So the banks started giving out homes to less responsible families, with zero down payment, no income certificate, nothing but just a formality of paperwork, and a promise of payback. They didn’t think of it as an issue because even if the families don’t pay, investors will own the house, which is also a great asset until there are so many houses for sale in the market.

In that situation, the ratings of those risky mortgage bonds would have gone down, right? But that didn’t happen. There was no one to ask the rating agencies how they were giving out the ratings. They were an authority in themselves whose ultimate aim was to impress their clients and earn money. The investment banks paid these rating agencies to rate their bonds and these agencies had no liability if their ratings proved wrong. They claimed the CDOs made by them had 90%+ AAA-rated bonds, but under the hood, it consisted of highly irresponsible homeowners who didn’t even deserve to get a $100 loan. So all these pieces of worthless junk bonds were bundled and sold as if they were gold, and no one bothered to look what’s inside. Investment banks were making profits by selling CDOs and agencies were getting paid for giving AAA ratings. Real estate prices skyrocketed as it was so easy to own one. A boom like this is called a Market Bubble– where everyone is so flattered with something in the market that they believe its demand will never go down and its value keeps on rising, even much more than its actual self-worth. But these prices are not more than an illusion created by fraudulent systems. These bubbles eventually burst and make a hard impact on everyone’s life. This time it was the Real Estate bubble in America that burst aloud in 2008.

Getting Insurance To The Crisis

The highly unregulated derivatives market of the USA allowed the bankers to gamble on anything. They could bet on the rise and fall of oil prices, bankruptcy of a company, or even the weather. Some of the psychopaths saw that the fall of the real estate was coming. So they introduced the Credit Default Swaps which were like insurance to the mortgage bonds. The buyer of these swaps will pay monthly premiums to the seller and the latter will pay colossal money to the former if the underlying mortgage bond defaults or fails. The demand for these swaps kept growing as more and more people realized that the housing market would crash. These swaps were packed in Synthetic CDOs.

So who was buying these swaps? The ones who were selling the underlying bonds. The investment banks were selling AAA-rated bonds in the markets and on the other hand, purchasing swaps on BB and BBB-rated bonds, as they knew the bonds would eventually fail.

Some highly corrupt officials even represented banks in the morning and the rating agencies in the evening. They packed the extremely risky bonds in the morning for the availability of bonds in the market and rated them 90% AAA in the evening for the investors’ sake. They also introduced a new complex derivative- a CDO of a CDO, called CDO Squared. The sole purpose behind their existence was to introduce more financial instruments in the markets, so there is always something to bet on. Let us see how they turned the whole world into a giant casino-

Suppose A and B are playing a game

C and D take a $100 bet on whom among A and B will win

E and F take a $1000 bet on whom among C and D will win

G and H bet on E and F

…. …. …. ….

There existed CDOs and synthetic CDOs as a bet against CDOs. Eventually, a $50 million investment had more than a billion dollars betting against it. The market for insuring bonds grew 20 times larger than the actual mortgage. The major players in this whole circus were investment banks like Goldmann Sachs, Morgan Stanley, Bear Stearns and Lehman Brothers, financial conglomerates like JP Morgan and Citigroup, securities insurance companies AIG, rating agencies like Moody’s, Standard & Poor’s, and many more. But from where was all this money coming? And how did they get the gigantic guts to borrow and invest? It was all possible because of the highly unregulated markets and the availability of cheap credit. Probably they all knew about the dangers they were playing with, but they also knew one more thing- they had grown so large that the government would have to save them if they go bankrupt, otherwise the economy would collapse. And that’s exactly what happened. The American taxpayer had to pay for all of their gamblings in the form of emergency guarantees and bailouts by the Federal Reserve. Several papers were published, a lot of people doubted about the crash, but nobody did anything tangible, not even the Federal Reserve.

You can now see how a system of billions and billions of dollars depended on a lie. Everyone was playing with a time bomb. This real estate bubble was about to burst and the whole world was about to hear it loud.

The Burst of The Bubble

When markets hit a little low in late 2007, people started to default on their mortgage and started leaving the houses. The number of these faulty people skyrocketed. The supply of houses in the market became much higher than demand, resulting in the breakdown of the prices. Now there was no sense in paying a $100,000 mortgage for the house worth only $90,000, even for those who were able to pay it.

Even well-off families started leaving their homes after taking their share, leaving the banking investors, small investors and lenders with a bunch of worthless properties. There was no more selling and buying of real estate in the market now as everyone knew it was useless. As every sector of the economy is deeply interconnected, the whole economy froze.

Companies like Lehman Brothers started filing for bankruptcy. Bear Stearns went out of cash. The stock market was on a bear run. The people had not seen the stock market steep so low in decades. People were thrown out of their offices in the peak hours of the day as their companies were no longer able to pay them. The so-called stock market experts were roaming on streets with their box of office essentials, which was now worthless.

The vast floors of Morgan Stanley and Goldmann Sachs, which used to trade billions of dollars a day, were now empty. The United States was no longer able to trade with other countries and the whole globe went into a recession that was never seen or expected in decades.

Five trillion dollars from the economy disappeared.

Eight million lost their jobs.

Six million lost homes.

And that was just in The USA.

Conclusion

In the post-crisis world, the government and the Fed should have taken responsibility for all the chaos and sent the gold plated corrupt bankers to jail. But nothing like this remotely happened. Instead, the so-called intellectuals blamed the small business people, laborers and employees as they always do.

The Fed and treasury department of The USA are still governed by the ones who were the crisis architects. The system never improved and the same things went on, only a bit modified to show everyone that they have changed.

Many major businesses in the globalized world are still void and it’s a bitter truth because that’s how the modern economies work. We may never know how many bubbles the global economy is having and how many of them have burst by the Covid-19 Crisis. We need to be aware of the lies in the market to keep our mind and soul together in times of these crises.

Majority of wealth in the world is with the minority of people leading to unequal distribution of money and issues such as poverty in society. As a solution to this problem, what if all the wealth in the world is divided equally among the people so that no one is poor and no one is rich. Sounds like an awesome and innovative idea, right??

First of all, the idea of equal wealth among the people will end competition. Competition is the force which thrives innovation, the development of new ideas, new products, services, and thereby development of economy and society. Competition improves the intellect of an individual and a whole society . The hunger for betterment and wealth creation; to be the best in class is what improves systems and makes any society futuristic. For an analogy, let’s assume a class of students. For this particular class, it is decided that whatever marks the students will get, it will be averaged and equal marks will be given to each student. In this scheme, the capable students will not put extra efforts, study and learn as they know this will not come to them in a whole whereas the incapable will become idle & lazy thinking that the others are doing their job for him & that he need not do anything . This will lead to deterioration of one’s intellect, lack of knowledge and skills.

In such a system, ingredients essential for development of an individual and a society such as ambition, hard work, dedication, excellence, ethics, etc. will not exist. An industrialist and a beggar have a huge difference in the mindset. An industrialist will invest the excess money in various industrial sectors and workforce giving employment to people whereas a beggar will simply spend the excess money relentlessly. If all the people have the same purchasing power, this will lead to inflation for a few ranges of products and others will lose their value and importance in the market. This will have a very bad effect on the cash flow in the markets. For maintaining global peace one of the essential factors is monetary power so that people can be led in some direction. The concept of equal wealth among all destroys this power.

The above ideology of equal wealth among all will require an enforcing organisation for its implementation in the long run. This is because it is impossible to make every person walk on the same principle; the monk principle (give free service to the society and to be satisfied with what one has).

Implementing the above ideology will decrease the value of money, deteriorate lifestyle and will lead from social equilibrium to a worldwide chaos. Hence, this ideology of a chaotic state is not applicable to the real world.

Brexit was a word barely heard till 2012 but rose to prominence and became a politically defining term in 2016. This term is a blend of two words “Britain” and “exit” which represents Britain’s exit from the European Union. Visionary leaders came together to create economic and political stability to ensure long term peace in Europe.

The EU had a total of 28 European member states, including the UK. From then on, many others have followed in their footsteps, striving to build on this vision through successive treaties. In 1957, France, West Germany, Belgium, Italy, Luxembourg, and the Netherlands signed the Treaty of Rome, which established the European Economic Community (EEC), the predecessor of today’s European Union.

The Treaty of Maastricht signed on February 7, 1992, established the European Union (EU) based on three pillars: the European Communities, the Common Foreign and Security Policy (CFSP), and the Police and Judicial Cooperation in Criminal Matters (JHA). It introduced the concept of European citizenship, enhanced the powers of the European Parliament and launched the economic and monetary union (EMU). The Treaty of Nice, signed in 2001, streamlined the institutional system in a bid to maintain efficiency. The UK finally made it into the club in 1973, but just two years later was on the verge of backing out again.

In 1975, the nation held a referendum on the question: “Do you think the UK should stay in the European Community (Common Market)?” The 67 percent “Yes” vote included most of the UK’s 68 administrative counties, regions and Northern Ireland. In contrast, only Shetland and the Western Isles voted “No.” The center-left Labour Party split over the issue, with the pro-Europe wing splitting from the rest of the party to form the Social Democratic Party (SDP).

Tensions between the EEC and the UK exploded in 1984 when the Conservative Prime Minister Margaret Thatcher talked tough in order to reduce British payments to the EEC budget. In October 2016, Prime Minister Theresa May announced her intention to invoke Article 50 of the Treaty on the European Union, formally giving notice of Britain’s intent to leave the EU. In the vote of June 23, 2016, The UK voted to leave the EU by 52% to 48%. Leave won the majority of votes in England and Wales, while every council in Scotland saw Remain majorities. On March 29, 2017, the order, signed by May was delivered to the Council of the European Union, officially starting the two-year countdown to Britain’s EU departure, set for March 30, 2019.

GBP’s (Great Britain Pound) roller coaster ride on Brexit

The economic relationship of Britain with the world was sure to take a different turn as it decided to leave the European Union. The boat of Brexit has posed many unforeseen challenges to the pound. Enhanced periodic volatilities have inevitably surrounded vital diplomatic and political events not just in the UK, but almost the entire European continent Let us witness the journey of pound through the Brexit years: –

JUNE 2016: BREXIT VOTE

The vote was undoubtedly an iffy prospect for political leaders and parties, economists and financial professionals. The aftermath of the March 2016 vote resulted in a tumultuous position of pound in the market. GBP experienced heavy losses and fell to a 31-year low. It continued to fall against its major standard competitor dollar in the coming months. It fell to 6% against USD in October 2016, and by June 2017 it had plummeted to a 12% low. That means the pound which was earlier worth 1.32 euros had fallen to a lowly 1.11 Euros by the October following the vote.

MARCH 2017: ARTICLE 50 IN PLAY

Because of the March 2017 triggering of Article 50, the GBP experienced considerable pressure after a Parliamentary vote cleared the way for May’s declaration. In the hours after Parliament rendered its decision, the GBP rapidly fell 0.7% against the USD.

DECEMBER 2017: EU/U.K. DIVORCE DEALS

On December 8, 2017, leaders from the EU and UK reached an agreement for the coming “divorce” or separation.

The deal outlined provisions for the Northern Ireland border, EU/U.K. citizenship and a financial settlement of £39 billion to be paid by the UK to the EU. Upon public announcement of a deal, the GBP rallied 0.9% against the USD and more than 1% vs the euro.

While some were apprehensive of the future of the pound, some people and organizations viewed this in the positive light. Analysts at Goldman Sachs said that the pound was still a profitable investment. Currency traders were also optimistic about the divorce move. The dubious atmosphere persisted, but GBP restored some of the trust, its potential in the global market soared again.

JANUARY 2019: REJECTION OF THERESA MAY’S DIVORCE DEAL

On January 15, 2019, the House of Commons officially rejected May’s divorce deal by an overwhelming margin. However, the vote came as no surprise to forex traders. For January 15, 2019, session, the GBP lost a modest 0.01% vs the USD while climbing by 0.46% against the euro.

There were possibilities of a new Brexit referendum, snap election or delay of the scheduled March 29, 2019, Brexit Day.

THE IMPLEMENTATION PERIOD

The “implementation period”, was the period of 21 months between March 29, 2019, and December 31, 2020. Many see the implementation period as merely being an extension of UK membership in the EU. However, the ability of the UK to negotiate its treaties opens the door for new economic partnerships. The GBP echoed this sentiment shortly after the Brexit transition deal’s announcement. Significant rallies against the euro (+0.51%) and USD (+0.61%) occurred after the agreement became public in March 2018.

However, the GBP struggled to sustain market-share throughout the tumult of 2018. For the year, the GBP lost 1.8% against the USD and 1.1% vs the euro. Nonetheless, the pound sterling rebounded in 2019 against the majors. During 2019, the GBP gained more than 4% and 6% versus the USD the euro respectively.

THE PRESENT AND THE FUTURE

There has been a diverse division of people of what holds for the UK economic future. People of the United Kingdom feel that leaving EU has saved the nation from various anomalies of the organisation like:

The corruption in the EU

Regional Separatist mentality in the number of member states

Anti-Democratic nature of EU

Experts say that leaving the EU might be the right decision in the long run. However, it leads to tensed relations with Ireland, losses for both, importers and of course, fall of the pound.

Being a part of the EU gave Britain a myriad benefits. However, its exit has put doubt in the mind of investors and businesses across the world. The UK was one of the politically most influential countries of the total of 28 countries. As it has withdrawn, there is speculation that Germany might rise to power and dominate the organization.

The bigger question which arises now is how Britain withdraws from the European Union, whether it will go for Hard Brexit (sharp deal to cut off ties with no trade and projects continued) or Soft Brexit (agreement on specific policies).

The coronavirus pandemic has already severely hit finances all over the world and the UK has taken one of the biggest hits by its GDP plummeting by 20.4%. It is undoubtedly a critical time for policy-makers and citizens all over the UK as their calculated risks and visions today will either save or destroy, once a valiant colony as the British empire.

If the UK fails to strike a deal with the EU by the current end date of the transition period, i.e., December 31, 2020 – and the period unextended – then the country would leave with no deal and revert to WTO rules on trade and security – which would have a direct impact on the pound.

Reading Time: 2minutesThe corona pandemic has claimed many lives across the world. It’s other side effects include the widespread rampage on all sectors of economy of the world. It has caused the closure of many small industries, businesses and enterprises and it continues to haunt the future of not only SMEs(Small and Medium Enterprises), MSMEs (Micro Small Medium Enterprises), Microfinance Institutions but also big companies.

In view of this, big Chinese banks, Private Equities and other multilateral instruments are investing heavily in such falling companies. These Chinese corporations work under the beneficial owner; the government of China. China’s recent increase in investment in HDFC bank has exceeded 1% which has poked the bear (RBI) into looking into this matter.

ATTRACTING INVESTORS IS GOOD, SO WHATS THE PROBLEM?

The problem is that by investing heavily they are buying shares of these companies at “THROWAWAY PRICES”. The impact of this, is that they will be majority stakeholders of these companies or aim to attempt buying them eventually (“HOSTILE TAKEOVER”). This will give them power to control these businesses and help them direct profit money to China.

China currently invests around $4 billion in Indian startups.18 out of 30 Indian unicorns (startups having more than $1 billion market capitalization) have Chinese funding.Big investors from China -Alibaba, Tencent , ByteDance have made huge investments in Paytm, Byju’s , OYO, Ola, Big Basket, Swiggy, Zomato. China dominates Indian markets in pharmaceutical APIs(Active Pharmaceutical Ingredients), mobile phone markets, automobiles and electronic and project imports.

HOW IS THE DRAGON’S MARKET INVASION BEING STOPPED?

The Government of India and RBI (Reserve Bank of India) lost no time in rectifying it’s policies.The government has decided to screen Foreign Direct Investments (FDI) from countries sharing a land border with India or where the beneficial owner of an investment into India is situated in or is a citizen of any such country. The capital market regulator of India ,SEBI (Securities Exchange Board of India) is also digging deeper into Foreign Portfolio Investors(FPI) composition from China, by seeking beneficiary details from jurisdictions like Mongolia, Bhutan, Nepal, Bangladesh , Afghanistan and Yemen.

SO WHAT’S NEXT?

These policy changes have put an end to such hostile takeovers yet other measures need to be taken in order to mitigate China’s sway over the market.

Since this concept is unknown to a lot of non-finance grads, I’ll try my best to cover the topic as quickly as possible, and yet make it explainable. We all have some dreams about how we’re going to spend our lives. And most of these dreams may require us to be financially sufficient, if not rich. And when I say that, I am sure everyone thinks about either starting-up something or investing. Here we’re going to focus on the later. Everyone knows the importance and benefits of investment, and types of financing options available for any investment. Sadly, while many have mentally accepted they’d want to invest when they start earning, a very few know how to! Modern Portfolio Theory, henceforth referred to as MPT, is the starting point to understand the world of investments, mathematically. Harry Markowitz suggested the MPT in 1952 for which he won the Nobel Prize in Economic Sciences later.

Understanding the parameters of MPT

MPT is an entirely risk-return based assessment of your Portfolio. This means all it looks for is how to maximize your returns for a given amount of risk. It assumes that different people have a different risk-taking attitude. A young person would be willing to take a greater risk if it might generate him greater returns. While someone who is old, would not be willing to take higher risks and would remain satisfied with lower returns. Whatever the risk attitude, it tries to search for the ‘combination’ of assets in the Portfolio that would generate the highest possible returns (for some risk). I hope we are clear with the very basic idea of what MPT is. Now let’s briefly understand how MPT defines risk and return for its assessment. According to MPT, returns are simply the profit you make on an asset over a period of time. It would be negative in case of a loss. Obviously, this is very much intuitive.

Mathematically, R is the percentage change in the value of assets.

R = [(V – Vo)/(Vo)]X100

Risk, according to Markowitz, can be expressed using the standard deviation of returns over a period of time. Recall from your high school statistics, the standard deviation is the measure of how deviated the values are from their mean. So, the logic here is, if the returns more largely deviate from their mean values, the asset having those returns is more volatile. More volatility naturally means its riskier. Look how I emphasized on ‘according to Markowitz’. This is because, there are several methods of risk assessment (eg. VaR, CVaR, Conditional Risk, etc). This is because different people have different notions of what risk means to them. For some, it is how large their return could be on the negative side. For some, by what probability they can suffer an X% of loss on a standard normal distribution of their returns (essentially, the Z-Score). Anyway, to understand MPT, we need the basic definition of risk as described by Markowitz.

Mathematically, Risk (σ) = std(returns over that period)

Now, this is how we can calculate the risk and return of an asset. But obviously, we are not going to invest in a single asset. So more important value to us is the risk and return of your entire Portfolio. Consider a portfolio with N number of assets.

The expected return Ro on each one of these N Assets is the average of per period return R calculated using the percentage change formula discussed before.

R0(single asset) = mean(R of the asset)

Now that we have net expected Return for each of N assets, the net returns of the Portfolio as a combination of all the assets is simply the weighted average. Its obvious, isn’t it? Return is a linear quantity. So if W1, W2, W3,..Wn are the weights of investment done in each of the Assets, the Portfolio Return (π) is,

π = mean(W.R) ∀ N assets.

Pretty easy right? Now, what would be the risk of entire Portfolio. Weighted average of the individual asset risks? NO! Remember, risk isn’t a linear quantity plus, the net risk of entire Portfolio will also depend on how one asset moves relative to the rest in the Portfolio. Example, it is generally observed that when markets plummet, gold prices soar (because gold is universal in its value, and people trust it more than cash). Hence if the equities in your Portfolio go down, the gold will rise. We can see a co-dependence of assets with each other, which will also influence the risk of the entire Portfolio. Hence mathematically,

σ(portfolio) = ΣΣ(Wi.Wj.σi.σj.ρij) ∀ i,j in N

where, ρ(i,j) = correlation between ith and jth asset.

The quantity σi.σj.ρij is also called Co-variance, σ(i,j). Now that we’ve understood the parameters of MPT, let’s get into a very easy and beautiful way to analyse portfolios – graphs.

The Risk-Return Space

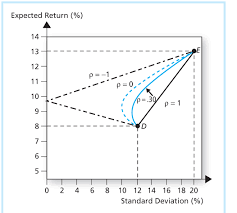

The best way to understand and portfolios is to plot the risk and return of each portfolio for a variety of weights W1….Wn, and choose the perfect one for your needs. That ‘perfect’ Portfolio would be the one providing the highest return for a given amount of risk. For a 2-Asset portfolio, the risk-return space looks something like this –

Look how different correlation values between the assets changes the portfolio curve. This curve is plotted by changing the weights assigned to each Portfolio, W1, W2. where W<1 and W1+W2=1 As the weights are changed, the portfolio return and risk change and hence the curve. One beautiful observation which is the heart of Modern Portfolio Theory, is that as the correlation approaches closer to negative values, the return one can get for a particular amount of risk increases. This is because less the correlation more differently, the assets will move respect to each other and as it turns negative, they essentially would move opposite to each other just like the gold-equity example discussed before. So far, so good. What happens to the curve when there are more than 2 assets. Now there wouldn’t be a single curve connecting 3 assets as in 2 asset case. This is because for every point on the curve between Asset A and B and Asset B and C, there would be an another portfolio X and Y. Hence the risk-return plot in any case of N>2 will actually be a space and not a simple curve.

The Efficient Frontier

This is an algorithmically generated Portfolio Space for 4 Assets and 1000 different portfolios constructed by altering W1, W2, W3, W4 such that each is less than 1 and sum is 1.

Look at the above space plot carefully. Keeping in mind that one would always be looking to invest in portfolios with a higher return for certain risk. We get a series of portfolios which would be ideal for us if the above condition is considered that is more return for a particular risk. That will be achieved if we invest on any point on a unique curve such that the curve represents the highest possible return for some risk. This curve will be the yellow curve plotted with space. Hence as long as you’re on the upper part of yellow curve, you’re an efficient investor. This curve, as described by the MPT, is termed as the “Efficient Frontier”. The efficient frontier development mathematically is a quadratic convex optimization problem here solved using python’s SciPy library with its convex optimizer. We will, in later blogs, discuss how we can use python to generate this efficient curve along with the portfolio space.

Conclusion

We come to the most beautiful conclusion in the world of Finance. There are a unique set of portfolios which offer you more return for risk as compared to other possible portfolios. Now go back and imagine you being an independent investor having X amount of money wanting to invest in N Assets. Instead of randomly listening to news, people or read articles, you now have trusted mathematical way to construct a perfect portfolio to plan for your dreams.

Hmm. But if this were so easy, everyone would have learnt MPT and made money. But that’s not the case. Probably there are some caveats to it too. This and a lot more in the following blog. Until then keep following CEV Blogs!